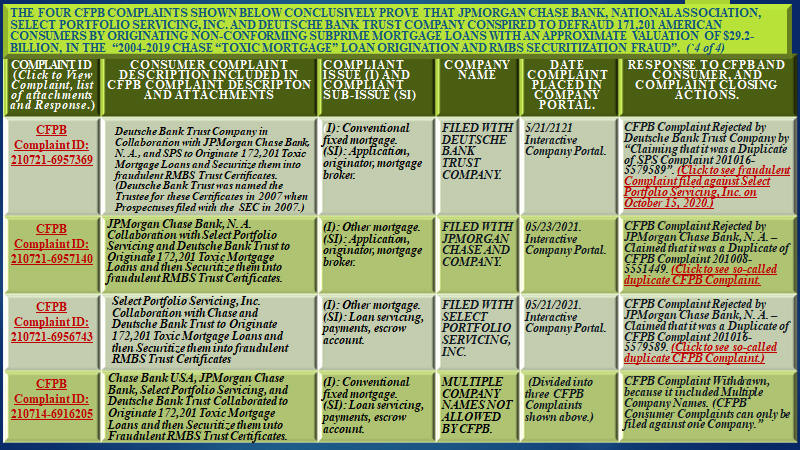

COMPANY-CENTRIC DESIGN OF THE CFPB COMPLAINT PROCESS:

"THE COMPANY" CONTROLS THE CFPB COMPLAINT ARBITRATION PROCESS, AND

CFPB TAKES NO ACTIVE ROLE IN THE CONSUMER COMPLAINT RESOLUTION

PROCESS!

HOWEVER, CFPB ALWAYS BLINDLY ENDORSES "THE COMPANY'S" ADJUDICATION

RESPONSE WITH ITS

KISS OF DEATH APPROVAL

AND THEN CLOSES THE COMPLAINT BY BANISHING IT TO THE CFPB COMPLAINT

"BLACKHOLE,"

FROM WHICH IT WILL NEVER ESCAPE.

CFPB plays no role in the COMPLAINT

ADJUDICATION PROCESS: "THE COMPANY" IS THE JUDGE,

jURY, AND APPELLATE!

FINANCIAL

SERVICES INSTITUTIONS, NATIONAL BANKS, and others ARE CURRENTLY

LOBBYING FOR THE SHUTDOWN OF THE CFPB COMPLAINT SYSTEM, BUT THEY DO

NOT REALIZE THAT "THEy" WINS MORE THAN EIGHTY PERCENT OF THE

COMPLAINTS FILED BY CONSUMERS; AND THAT CFPB, RUBBER-STAMP'S "theIR"

response more than ninety-three percent of the time! "THE COMPANY"

CURRENTLY HOLDS ALL THE CARDS, AND ARE THE PROVERBIAL: "JUDGE, jURY,

AND EXECUTIONER" OF COMPLAINTS RECEIVED VIA THE CFPB COMPLAINT

PROCESS.

Current Initiatives by some large

financial services companies, and national banks to weaken (or even

abolish) the CFPB Consumer Complaint process, is the classic example

of: "Killing the Golden Goose"; because as of April 2017, the more

than seven hundred and forty-three thousand consumer complaints

contained in the CFPB Complaint Database, shows that: "THE

COMPANY ALWAYS WIN!" Some of the many glaring examples that

corroborate this hypothesis include:

-

The CFPB Complaint Process includes an "INSIDIOUS

ALL-SEEING, ALL-KNOWING COMPANY PORTAL" by which it

connects to more than four thousand financial services

companies. This omnipresent portal is not mentioned in

any consumer-related documentation; even though it,

along with the CFPB Complaint Database, underpins the

CFPB Consumer Complaint process. The "portal" is a

web-based, interactive information channel between CFPB

and "The Company"; and

-

Although the CFPB Complaint Process documentation still

includes terms such as "sending CFBP complaints to The

Company" or uploading complaint data to "the Company,";

the reality is that all of the more than forty-two

hundred registered companies have instantaneous access

to CFPB Complaint data residing in the Company Portal,

and; this "all-seeing, all-knowing portal" provides the

"The Company" with instant, real-time access to all CFPB

complaints filed by consumers; thus, it can re-use

arbitration responses that it previously used for

similar complaints, as well as "canned" responses such

as: a.) we have yet responded to this issue, b.), please

contact your servicer regarding this issue and c.) we do

not discriminate.

-

These companies

are solely responsible for the arbitrating and closing

all consumer complaints they received via Company

Portal, and;

-

CFPB "Rubber-Stamped" the Company responses, more

than 93% of the time,

-

More than seventy-three percent of all consumer

complaints are "Closed with Explanation," by the

Company; with no "Monetary Relief" for the consumer,

and;

-

The annual ranking of Companies based upon the number of

complaints received, percentage of complaints "Closed

with Explanation," and percentage of complaints "Closed

with Monetary Relief', are not shared by CFPB, and;

-

More than ninety percent of the Company responses

to consumer complaints are not publicly shared,

and this allows many the Company to reject, and

"Close without explanation," more than ninety percent of

all CFPB consumer complaints received, without drawing

the attention of other federal or state consumer

protection/consumer complaint agencies, and;

-

There is no dispute or escalation procedure available to

consumers who disagree with the response received from the

Company, and;

-

For all intentional purposes, consumers who filed

complaints with CFPB, and had their complaints rejected

and closed by the Company;

inadvertently-eliminates all future options of filing

the same complaint with CFPB, or other federal, state,

or local consumer protection/consumer complaint

agencies, and;

-

The CFPB "Stamp of Approval" of the Company

response, can be referenced by the Company, in

its responses to future CFPB complaints from the same

consumer (or other consumers), and, finally;

-

Other federal consumer complaint agencies, such as the

Consumer Assistance Group (CAG) of the Office of the

Comptroller of the Currency (OCC), continue to refer

consumer complaints (i.e., "Blindly throw consumer

complaints over-the-wall") to CFPB, even though they

have been alerted again, and again, and again of dozens

of architectural and process flaws in the CFPB Complaint

Process.

Click

HERE view more

details regarding the Company-Centric CFPB Complaint

Process.

The CFPB's: "The Company is Always Right Approach", to

resolving consumer complaints, is an overt, blatant

contradiction to CFPB fiduciary responsibility as defined in

the Dodd-Frank Wall Street Reform, and Consumer Protection

Act of 2010. This Act empowered CFPB with the responsibility

to ensure that financial-related consumer complaints, filed

by American consumers, were arbitrated on a fair and

impartial basis.

|

"THE COMPANY

ALWAYS WINS!"

THE CFPB COMPLAINT

DATABASE SHOWS THAT The ratio of Consumer Complaints "Closed with

Explanation" versus Consumer Complaints "Closed with Monetary

Relief" is more than 10:1 for all COMPLAINTS; AND AS HIGH AS 30:1

FOR MORTGAGE-RELATED COMPLAINTS.

During the period in question from

between January 2012 and April 2017, the CFPB Complaint Database

shows that:

-

553,374 (74.44%) of the 743.427 consumer

complaints were "Closed with Explanation" by the

Company, and;

-

49,609 (6.67%) of the 743,427 consumer

complaints were "Closed with Monetary Relief" by the

Company.

As incredible as the

above "Closed with Explanation" responses from Companies

are; the "Closed with Explanation" responses for Mortgage

complaints are even higher:

-

157,316 (89.42%) of the 175,934 consumer

mortgage complaints were "Closed with

Explanation" by the Company, and;

-

4,952 (2.81%) of the 175,934 consumer

mortgage complaints were "Closed with Monetary

Relief" by the Company.

-

This is a 31:1 ratio of Closed with

Explanation versus Closed with Monetary Relief

responses from the Company. (Click

HERE for

additional Top-10 mortgage complaint

statistics.)

|

Additionally, between January 2012 and April

2017, consumer disputed 145,150 (19.5%) of the 743,427

responses received from the Company; and apparently, none of

these complaints resulted in further actions upon the

consumers' behalf by CFPB. (It is important to note; that

the CFPB Freedom of Information Act (FOIA) Office disclosed

that CFPB referred 21,198 consumer complaints to other

agencies during the period in question; however, because

these referrals were not tracked in the CFPB Database, it is

unclear if these referrals were based upon consumer

complaints or CFPB actions. (A summary of these CFPB

Referrals can be viewed

HERE.)

|

Other

Major Problems Found in Flawed-CFPB Complaint Process

Some of the most glaring problems we found within the CFPB

Complaint Process include:

-

Companies are allowed to

arbitrarily close complaints even though consumers

have formally disputed the Company Response. In most

instances, the consumer's disputes include

additional documentation that further authenticates

and/or strengthen their original complaint. Between

2011 and March 26, 2017, consumers disputed more

than one hundred and forty-five thousand Company

responses, and there are no records in the CFPB

Complaint Database that any of these disputes were

ever reviewed by CFPB Reviewers, before being

discarded. (Click HERE to see a list of all consumer

complaint disputes by Company, by year.)

-

The Company is allowed to specify whether, or not;

its response to a consumer can be shared publicly;

and if they choose to not share this information,

consumers have no awareness of similar complaints

filed by other consumers.(More than ninety-three

percent of all Company responses, were not shared

publicly. See table below entitled: "Company

Responses Sent to CFPB and Consumers, but not Shared

Publicly", to see annual percentages of Company

responses not shared publicly. (When Companies do

not share their responses to consumer complaints

publicly, it is virtually-impossible for consumer

protection agencies to track and analyze patterns of

potentially-fraudulent and/or criminal behavior by

Companies.)

-

Complaints referred by other consumer complaint

agencies, do not receive any special treatment, even

though they have already been reviewed before being

referred to CFPB; additionally, it does not appear

that the Company is made aware of the fact that

these complaints were review by another agency

before being referred to CFPB. Finally, when the

Company closes the complaint, the response by the

Company, is not forwarded to the referring consumer

complaint agency, and if another consumer files an

identical complaint, there is no ability of the

referring agency to inform this consumer of the

results of the prior complaint(s).

-

The CFPB Consumer Complaint Database includes

ninety-five issues, which can be used by consumers

to file complaints with more than forty-one hundred

companies; however, all of these issues appear to be

given the same CFPB ranking and/or priority. As this

implies, all of these ninety-five issues are treated

equally, in the CFPB complaint process; for example,

it appears that a five-hundred dollar pay-day loan

complaint is treated the same as a five-hundred

thousand dollar home mortgage loan complaint. (Click

HERE to see a list of all CFPB complaint issues.).

-

Complaints alleging

serious, and possibly felonious, violations of

federal and state laws are apparently handled the

same as all other consumer complaints, and

theoretically, there could be dozens, if not

hundreds, of similar complaints against a Company; and CFPB would

never refer any of these alleged criminal activities

to its internal enforcement unit, or to other law

enforcement agencies.(Click

HERE

to view all CFPB Consumer Complaint actions for

these Identity theft, Fraud, and Embezzlement

complaints.)

-

Click

HERE

to see the top-twenty reasons why the CFPB

Complaint Process does not work.

|

When a consumer Files A

COMPLAINT via the CFPB complaint process, it is frequently THE

PROVERBIAL "THE KISS OF DEATH" for not only that COMPLAINT; but

it virtually eliminates the probability that similar complaints

from other consumers will receive a fair and objective

arbitration!

Filing a consumer complaint against a Company

with CFPB, (or other federal agencies that, frequently and

unceremoniously, "throw consumer complaints over the wall" to CFPB), is

the proverbial "Kiss of Death" to the complaint. As the following

Mortgage Complaint table shows, in the vast majority of instances, the

Company simply rejects the consumer complaint, and sends a "Closed with

Explanation Response to CFPB; and then the Company is virtually-immune

to any future CFPB-related actions from the consumer. Furthermore, the

Company can explicitly-request that its response to this complaint not

be shared publicly, and then used the CFPB-approved "Closed with

Explanation" response, to respond to dozens, or even hundreds of

identical (or similar) complaints from other consumers. The fact that

the Company chose not to share these responses publicly, means that

consumers, and other consumer complaint/consumer protection agencies,

have no awareness of the fact that a given consumer complaint was

previously-filed with the CFPB dozens, in some cases hundred, of times.

|

Responses to Complaints against All Mortgage Companies |

|

Closed Response |

Year Complaint Filed |

Total Complaints |

Percent Complaints |

| 2013 |

2014 |

2015 |

2016 |

|

Closed |

1569 |

952 |

1177 |

882 |

4580 |

2.60% |

|

Closed with explanation |

42723 |

39286 |

37685 |

37622 |

157316 |

89.42% |

|

Closed with monetary relief |

1323 |

1050 |

1300 |

1279 |

4952 |

2.81% |

|

Closed with non-monetary relief |

3760 |

1633 |

2122 |

1571 |

9086 |

5.16% |

|

Grand Total |

49375 |

42921 |

42284 |

41354 |

175934 |

100.00% |

|

Source: CFPB Consumer Complaint Database

at:http://www.consumerfinance.gov/data-research/consumer-complaint |

| Although the almost ninety percent

"Close with explanation" response rate for all mortgage

companies is outrageous; "Close with explanation" responses from

other Top-10 Mortgage Companies are as high as 98.57%. Click

HERE to see more Close with explanation

responses from the Top-10 Mortgage Companies.. |

| REGARDLESS OF THE METHOD USED BY

CONSUMERS TO FILE COMPLAINTS VIA "THE FLAWED-CFPB COMPLAINT

PROCESS"; THE RESULTS ARE ALWAYS THE SAME, "The Company

"THE COMPANY ALWAYS

WIN!"

|

During much of the Twentieth Century, there was a

long-accepted axiom that "The Customer Is Always Right"; and

while this adage usually applied to customer complaints, and was

most prevalent within segments the retail industry; many other

industry segments, including the financial services and mortgage

lending industries, adopted this "golden rule" as a core

business principle. From the consumer's perspective, this

changed within the mortgage industry during the previous decade,

when this industry was inundated by hordes of new predatory

subprime lending institutions. In this new hyper-competitive

environment, even large financial services corporations, and

National Banks were "forced to bend the rules" in order to

remain competitive. The CFPB Consumer Database, used to create

this "Consumers for Consumers" website, vividly illustrates that

"The Customer Is Always Right" has been supplanted by a new

axiom that "The Company Always Wins". From January 1, 2012,

through March 26, 2017, the CFPB Complaint Database shows that

743,427 consumer complaints were submitted to the CFPB Complaint

Process. The origin of these consumer complaints were:

|

Email:

|

348 |

|

Fax: |

10,619 |

|

Phone:

|

51,038 |

|

Postal Mail: |

47,329 |

|

Referral from other agencies: |

130,671 |

|

Web: |

503,422 |

| Total |

743,427 |

The six-year history of the more than forty-one hundred companies to

which CFPB filed consumer complaints can be viewed:

HERE, and the

companies' responses to these consumer complaints viewed

HERE.

The Collaboration BETWEEN CFPB, AND other federal

Consumer Complaint Agencies VIA THE CFPB CONSUMER COMPLAINT PROCESS FACADE.

An analysis of the 2011 through

2017 consumer complaint contained in the CFPB Complaint Database

show that some Consumer Complaint Agencies, Consumer Protection

Agencies, and even Civil Rights Agencies, are not Fulfilling their

Fiduciary Responsibilities to American Citizens, by Indiscriminately

throwing Consumer Complaints "Over The Wall" to a Defective-CFPB

Consumer Complaint Process.

| In many instances, consumer complaints are "Blindly Thrown Over

the Wall to CFPB"; even though the CFPB Complaint Database

shows that the so-called CFPB Complaint Process allowed Companies

to prevail in more than Eighty Percent of all complaints filed

between 2011 and 2017. |

In 2012, during its first full year

of operation, CFPB received slightly over seventy-two thousand consumer

complaints; and the annual number of complaints received by CFPB has

steadily increased, to the point where there were more than one hundred

and ninety-one thousand consumer complaints processed in 2016. As this

rapidly increasing number of CFPB complaints illustrates, consumers have

become increasingly dissatisfied, and more cynical of the quality and

fairness of the financial products and services that they are being

offered; and are registering their displeasure, by filing complaints

with federal, state, and local consumer complaint agencies. However, the

spectacular successes claimed by CFPB have resulted in a "LET CFPB DO

IT" approach to resolving consumer complaints, and today, federal,

state, and local consumer protection agencies rarely pursue complaints

and/or claims against Companies, and virtually all federal consumer

complaints are thrown over the wall to CFPB. Our analysis of the Top-10

Companies to which CFPB filed consumer complaints shows that:

- The Top-20 Companies accounted for 94,428 of the total

130,671 referred complaints for all Companies, and;

- 15,935 of the responses to consumer complaints referred

to these Top-20 Companies were disputed by consumers. (Paradoxically, in May 2017, CFPB admitted that these

so-called consumer complaint disputes, were only used for

Consumer Feedback purposes, and played no role in the

consumer complaint process.)

|

Annual consumer complaint analysis of Top-20

Companies are shown in a series of tables below. Additionally, complaint

analysis summaries of: the

Top-10 Companies can be found

HERE;

and the Top-10 Mortgage Companies, by clicking

HERE.

NO Discrimination-related Complaints

are INCLUDED IN THE CFPB COMPLAINT DATABASE, AND ARE not supported BY CFPB Complaint Process!

CFPB WORK INCLUDE:

q

Rooting out unfair, deceptive, or

abusive acts or practices by writing rules, supervising companies,

and enforcing the law.

q

Enforcing laws that outlaw

discrimination in consumer finance.*

q

Taking consumer complaints*.

q

Enhancing financial education.

q

Researching the consumer

experience of using financial products.

q

Monitoring financial markets for

new risks to consumers.

*

Primary responsibilities of CFPB Complaint Process.

Although, one of the key drivers behind the Dodd-Frank Wall Street

Reform and Consumer Protection Act was to provide a fair, and equal

playing field upon which all consumers would have access to Fair Lending

and Equal Credit Opportunities. However, something was lost between the

enactment of this Act into law, because the CFPB Complaint Process, and

the CFPB Complaint Database are devoid of any mention of racial,

ethnicity, gender, or religious discrimination. The only demographic-type

information contained in the CFPB Complaint Database is: older

Americans, servicemembers, and older servicemembers; but it is unclear

iF this information was included in the complaints sent to Companies.

Click

HERE

to review the CFPB Credit Discrimination Policies. (This document can

also be found online under the heading: Addressing credit discrimination at:

https://www.consumerfinance.gov/about-us/blog/addressing-credit-discrimination/.)

Discrimination, in particular, racial

discrimination continues to be one of the greatest problems in

America; yet none of the ninety-six ISSUES included within the

CFPB complaint process, are for the multitude discriminatory

practices that exist within today’s US financial services

industry. CFPB was formed by the Dodd-Frank Wall Street Reform

and Consumer Protection Act of 2011; which was intended to

ensure that the American consumer had a mechanism for seeking

arbitration and mediation of their financially-related

complaints against predatory, fraudulent, and frequently

criminal practices of unfettered financial services

institutions, unregulated non-banks, regulated national

regional, and unregulated state and local banks. The following

seven points from the CFPB-own Credit Discrimination Guidelines,

makes it clear that this Act intended to provide a level

financial playing field for all American consumers, regardless

of race, ethnicity, gender, and religion.

-

Review lenders’ policies, procedures, and lending activity to detect

and address potential discriminatory practices.

-

Bring enforcement actions to stop discriminatory practices and

remedy harm to consumers.

-

Develop new policies, including rules about loan data collection

required by Congress. These data will help ensure that lenders make

credit available in a fair and non-discriminatory manner.

-

Partner with private industry and fair lending, civil rights,

consumer, and community advocates to promote fair lending compliance

and education.

-

Help ensure that consumers have the tools they need to make sound

financial decisions and protect themselves from discriminatory

practices.

-

Assist in reviewing consumer complaints of unlawful discrimination.

We can also review complaint patterns for early warnings about

troubling lending practices. This data will help us in our

supervision, enforcement, rule writing, and education efforts.

-

Conduct research and analysis on equitable access to credit. This

will include analyzing data collected under Federal regulations.

-

Work with the Department of Justice, Department of Housing and Urban

Development, Federal Trade Commission, and other federal and state

agencies to make sure that our fair lending enforcement efforts are

consistent, efficient, and effective.

However, it appears that something was lost

during the translation of the discriminatory credit policies listed

above, and the actual implementation of the CFPB Consumer Complaint

Process, because nothing in the more than seven hundred and forty-three

thousand CFPB complaints included in the CFPB Database, can be

specifically-associated with racial, ethnic, gender, or religious

discrimination. Additionally, during the six years that CFPB has

existed, none of the twenty thousand plus consumer complaints that have

been referred to other federal, state and local agencies, none have been

referred to the CFPB’s Office of Civil Rights, or the Civil Rights

Office within the Department of Justice.

"No Discrimination-Related Issues, or Sub-Issues, are

included in the Current CFPB Complaint Process!" *

It is highly probable that during the past six-plus years,

tens of thousands of consumers have attempted to file

discrimination-related complaints via the CFPB Complaint Process, alleging some form of racial,

ethnic, gender, age or religious discrimination; however, because

there are no discrimination-related "Issues or Sub-Issues"

within the CFPB Complaint Process, the only way these

discrimination-related claims can be sent to "the Company", is

in appended text-based narratives.

(Given "the

Company is A Right" biases ingrained in the CFPB Complaint

Process, the Company is only required to respond to the Issues

and Sub-Issues of the complaint; and thus, there are no

motivations for "the Company" to respond to appended consumer

complaint narratives.)

* See BUREAU OF CONSUMER FINANCIAL PROTECTION (Docket No.

CFPB-2012-0023) Notice of final policy statement for the

justification for not including discrimination-related data in the

CFPB Complaint Database.

Click

HERE

to see a summary of all Issues and Sub-Issues in consumer

complaints from January 2011 through April 2017.

Also, click

HERE to see a printable list of ninety-five Issues that are

included in the CFPB Complaint Process.

Read more regarding why "The

CompanyAlways Wins"!

|